Term deposits rates have risen in line with interest rates. But don’t discount bonds for longer-term outperformance.

Persistently high inflation has forced the Reserve Bank of Australia and other central banks to rapidly raise official interest rates, which has flowed through to fixed income (bond) markets.

The good news is that bonds now offer higher yields for income-starved investors. But term deposits available through financial institutions are also attractive for the same reason. Given the turmoil bond markets experienced in 2022, investors may feel term deposits are the safer and more rewarding alternative.

So, which is the better option? To answer this question, we need to take a long-term view of investment returns and asset allocation.

1. Bonds tend to deliver better returns

Term deposits can offer appealing short-term returns. But historical returns over longer periods reveal that bonds tend to offer better returns.

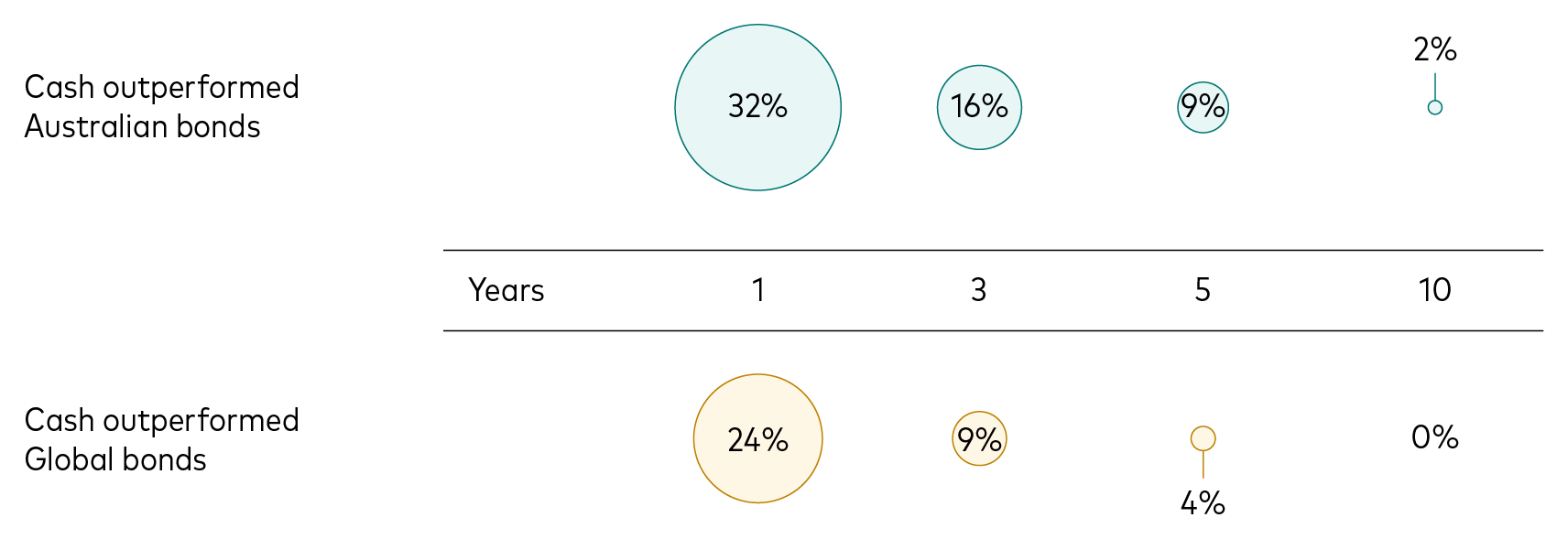

Using cash as a proxy for term deposits, we can compare rolling returns for cash and bonds over the past three decades (from the start of 1990 to the end of August 2023).

If we look at one-year rolling returns, we can see that cash outperformed Australian bonds 32% of the time. However, on a 10-year basis, cash outperformed only 2% of the time.

For global bonds, the story is even more stark, with cash having outperformed 24% of the time on a one-year basis and 0% of the time on a 10-year basis.

Bonds have delivered for long term investors: Percentage of time periods where cash beat bonds

Notes: Data reflects rolling total returns for the periods shown and are based on underlying monthly total returns for the period from January 1990 through July 2023. The Bloomberg AusBond Composite 0+ years and the Bloomberg Global Aggregate Bond Index (AUD hedged) used as proxies for Australia and global bonds respectively. AusBond Bank Bill Index is used as a proxy for term deposits.

Source: Lonsec irate generated 1 September 2023. Calculations Vanguard, as of 1 September 2023.

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance.

2. Bonds allow you to lock in yields for longer

Interest rate movements can create short-term volatility for bond portfolios. But reinvestment risk may pose a far greater threat to returns.

Reinvestment risk is a form of financial risk primarily associated with fixed income securities where there is a chance the cash flows received will be lower in future if capital is rolled over to a new fixed income investment paying lower yields.

Higher current yields on term deposits may seem like a great solution on the surface, but the level of rates and the shape of the yield curve do not move in predictable ways.

Starting yields are much less predictive of 10-year returns for short-term securities

Notes: The first chart shows the relationship between the starting yield on 3-month constant maturity T-bills and their subsequent 10-year annualised return. The second chart shows the same relationship, but with the starting yield on 10-year Treasury notes and their subsequent 10-year annualised return. Data as of June 2023.

Sources: Vanguard, based on data from the Federal Reserve Bank of St. Louis, Robert Shiller’s online data, and Global Financial Data from September 1981 through June 2023.

A practical benefit of favouring bonds over term deposits is that their yields tend to be more durable compared with bank bill rates.

The durability of long-term bond yields, especially over decades of investing, may improve the chances that investment outcomes will align more closely with longer-term goals. Choosing to focus on this long-term benefit is not always easy, but it’s worth it.

3. Bonds offer better downside protection

Bonds tend to be negatively correlated with equities over longer timeframes, meaning they offer a diversification benefit for portfolios. Even during periods when yields have been close to historic lows, bonds have offered diversification benefits when equity markets become turbulent.

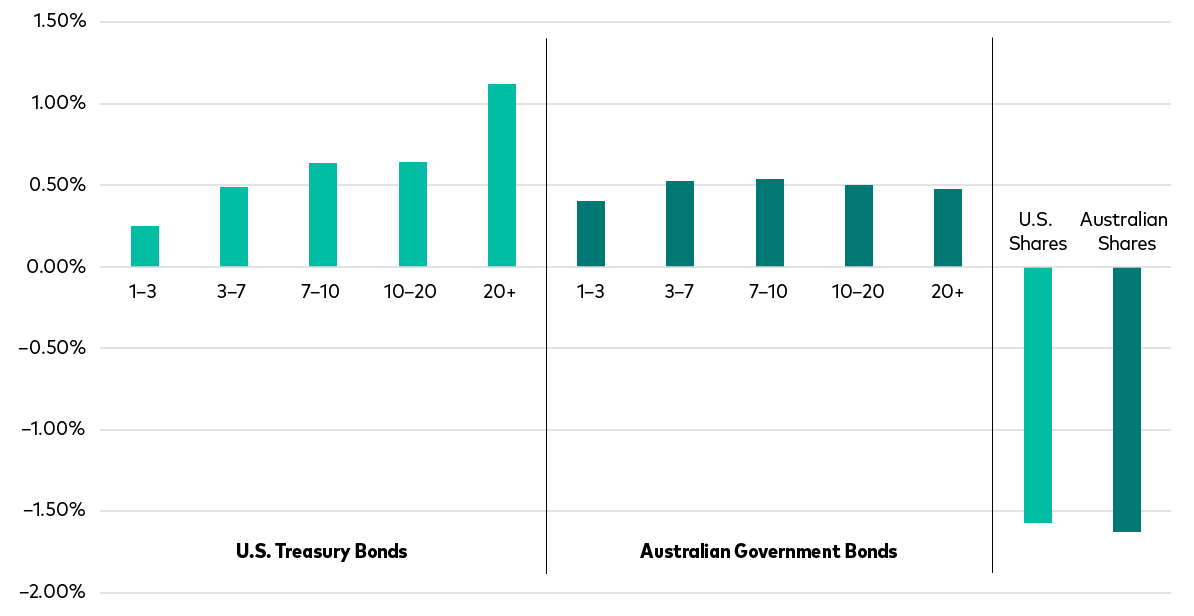

A diversified portfolio with broad fixed income exposure will include bonds with a range of different maturities. However, as the chart below shows, it’s worth including a significant allocation to high-quality bonds with longer maturities due to the diversification benefits they offer when equities head south.

Why invest in broadly diversified bond funds?

The monthly asset returns during periods of worst quartile equity markets for the respective Australian and U.S. markets – 20 years to 30 September 2023.

Source: Bloomberg and Vanguard calculations. Indexes used are Bloomberg U.S. Treasury and the S&P 500 Index, and the Bloomberg AusBond Australian Government Bond Index and the S&P/ASX 200 Index.

The diversification benefits of bonds are especially important during periods of economic uncertainty when the likelihood of a recession is high.

Diversification remains a cornerstone of sound financial planning. By incorporating bonds into a portfolio investors can achieve a well-rounded mix that positions them to navigate various market conditions more effectively.

Lock in yields while you can

In terms of bond market performance, 2022 was a highly unusual year.

It’s important not to use our rear-view mirror when making investment decisions. In 2023, bonds are behaving more normally, and yields are showing signs of stabilising.

Vanguard believes that most major economies are probably nearing the end of their rate hiking cycle, meaning now is a good time to consider having a high-quality fixed income exposure.

If a recession does arrive in the near future, we expect investment-grade bonds to hold up reasonably well and benefit from potential price appreciation.

As the tides of the market continue to shift, exploring the potential benefits of bonds in 2023 and beyond might be the strategic move that enhances your overall portfolio performance.

Feel free to contact our investment team to find out how we can help you reach your financial goals. Give us a call at 08 8231 4709 or send us an email at info@centrawealth.com.au.

Article courtesy of Vanguard.